![How to Avoid Overdraft Fees [8 Ways]](https://i0.wp.com/qualifylearner.com/wp-content/uploads/2025/05/How-to-Avoid-Overdraft-Fees-8-Ways-150x150.jpg "How to Avoid Overdraft Fees [8 Ways]")

Best for First-Time Advice Seekers

Financial Advice

- Free 45-minute call with a real advisor

- Personalized, judgment-free advice

- No pressure to sign up or continue

- Fast, easy scheduling

- You don’t choose your advisor

- Ongoing support isn’t free

Financial advice can feel out of reach, like something reserved for people with trust funds or tax headaches. But what if you could just talk to someone? For free. No pitch. No pressure.

That’s the idea behind Money Pickle, a service that matches you with a vetted advisor for a 45-minute call. I tried it myself, half-expecting a sales trap—but I walked away genuinely impressed. Here’s what the process looked like, what we talked about, and why I’d actually recommend Money Pickle (even if you think you don’t need financial help).

Table of Contents

What is Money Pickle?

Money Pickle is a free service that matches you with a real financial advisor for a 45-minute call. The whole mission is to make financial advice more accessible, especially for people who aren’t sure where to start.

Instead of cold-calling firms or Googling “financial advisor near me” to find a financial advisor online, you just answer a few questions and get matched with someone who fits your situation.

Every advisor is a Certified Financial Planner (CFP®), and the conversation is designed to be just that—a conversation. You talk through your goals, get a second opinion, and figure out whether working with a pro makes sense for you.

For anyone who’s unsure whether they even need a financial advisor, Money Pickle is one of the easiest ways to find out.

How does Money Pickle work? A step-by-step walkthrough

Here’s exactly what happened when I signed up for Money Pickle, from booking the call to joining the meeting.

Booking the call

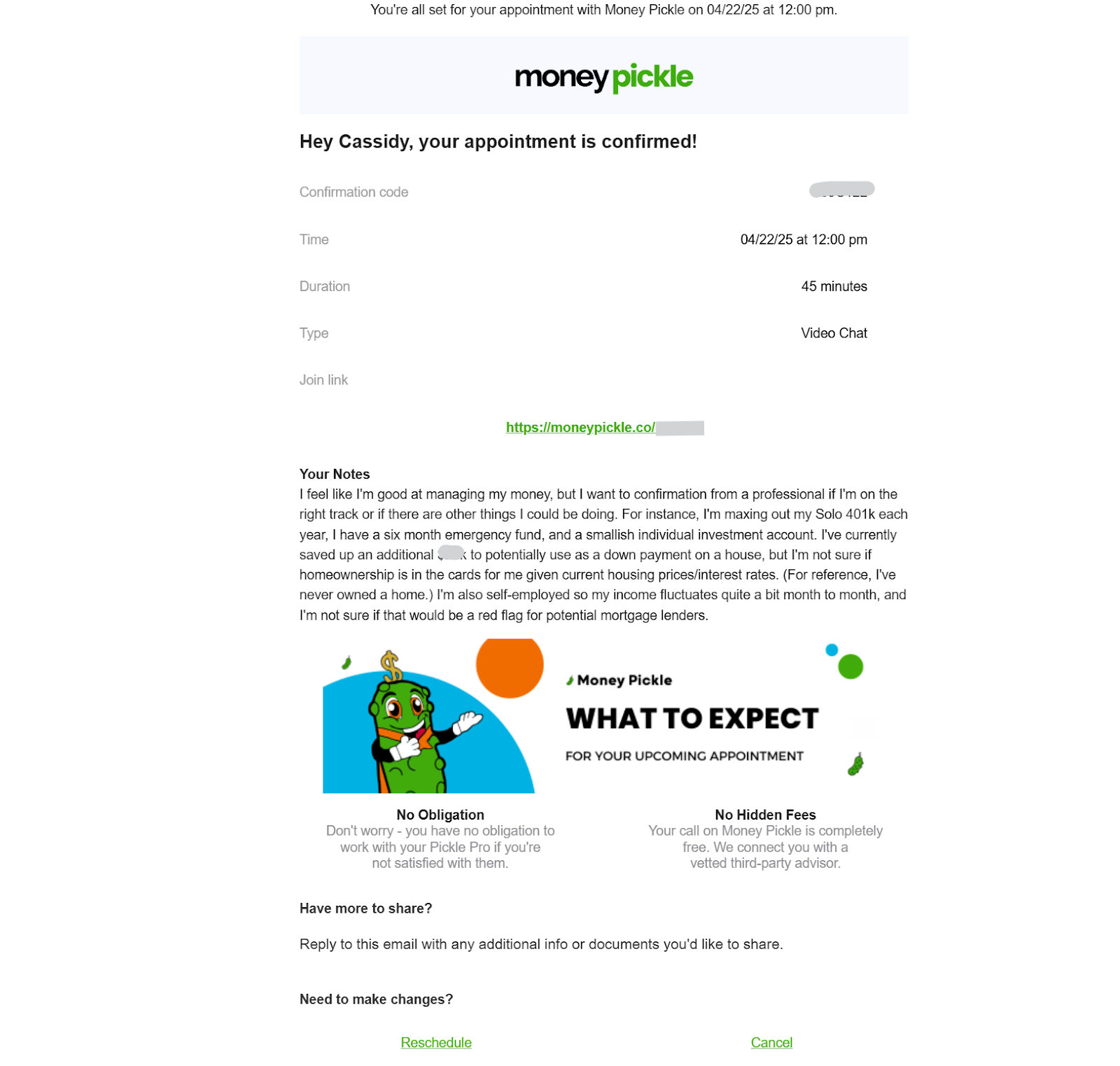

It took less than 10 minutes to book. After answering a few questions about my income, savings, goals, and what I wanted to discuss, I could browse open time slots. There were plenty—almost every day and time was available. I picked a slot two days out.

Right after booking, I got a confirmation by text and email (screenshot below). One heads-up: I booked while in a different time zone and accidentally scheduled the call for Mountain time instead of Pacific. Totally my error, but something to watch for.

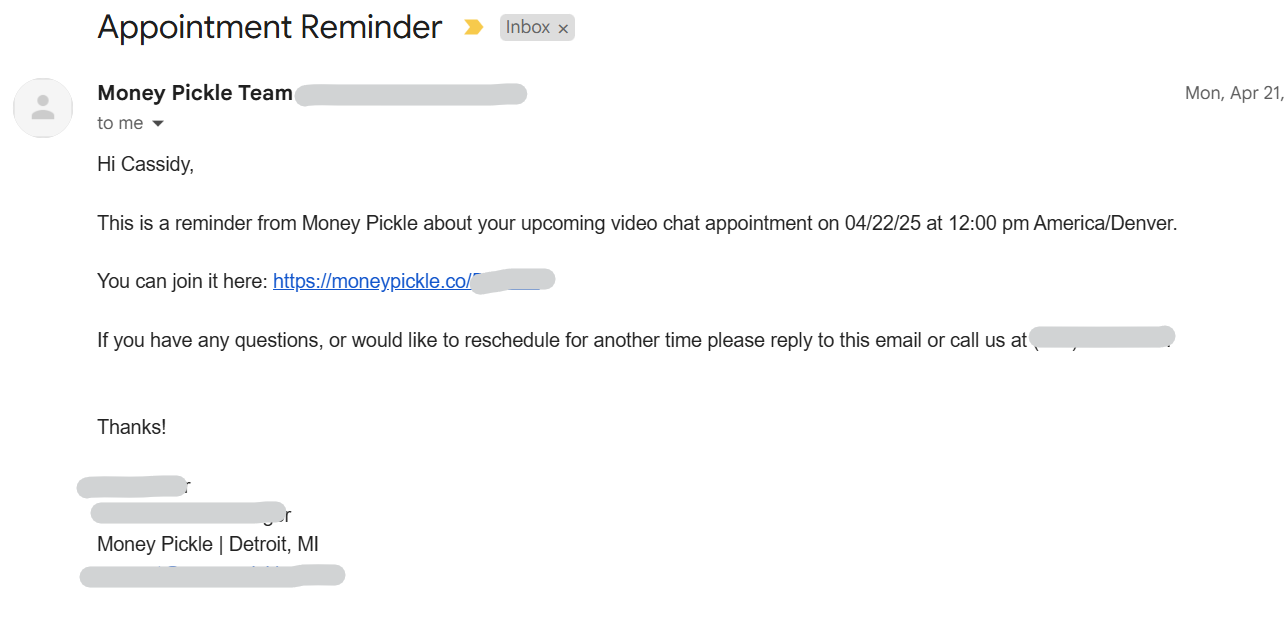

Pre-call reminders

The day before, I got a text, email, and phone call reminding me about the meeting. The email included a calendar link and video call info. It was all super clear and professional. Nothing felt last-minute or clunky.

Intake form

The intake form I filled out before booking my call asked thoughtful questions about my current financial picture and what I hoped to get out of the call. It wasn’t long or overwhelming, but detailed enough to give the advisor a head start. I could tell later that my advisor read my responses, which made the conversation feel personalized from the start.

What happened on my Money Pickle call

When I joined the call, my advisor was already waiting. He was based in the Denver area and came across as thoughtful, warm, and extremely prepared. He asked follow-up questions about specific items I’d mentioned in my intake form, which made the conversation feel personal and intentional.

I told him I already felt confident about my finances. I max out my retirement accounts. I have a fully funded emergency fund. I track my spending. I just wanted a professional gut check. Was I missing something? Was there a smarter way to do what I was already doing?

Then I shared my biggest question

I have $50,000 saved for a down payment on a home, but I’m genuinely unsure whether I want to buy. Would it even make sense for me? And if not, what should I do with that money instead?

His answer was one of my favorite moments of the call. Instead of rattling off generic pros and cons, he framed it as a values-based decision. Then he got more specific, suggesting I compare the cost of renting versus buying in my area to see which aligns better with my long-term goals.

He also pointed out that buying might only make financial sense if I plan to stay in the home for at least seven to 10 years, especially in this market. But if it makes emotional sense, that’s a whole other story.

Another insight that stopped me in my tracks

He noticed that as an S-corporation owner, I pay myself a relatively modest W-2 salary. But employer contributions to a solo 401(k) are capped at 25% of W-2 wages.

Meaning: if I slightly increased my salary, I could save more for retirement, which would also help me lower my taxes. That’s something I hadn’t thought about or read anywhere else.

The best part? There was zero sales pressure during the call. He didn’t bring up fees, didn’t push me to book again, didn’t try to sell me on a service. He said my second meeting would also be free, and that if I ever did want to continue, we could talk about what that might look like.

A few hours after the call, he followed up with a recap email outlining everything we discussed—plus a gentle invitation to continue the conversation.

How much does Money Pickle cost?

Money Pickle itself is completely free. You don’t even need to create an account.

If you decide you want to keep working with the advisor after your free call, that’s when pricing comes into play. But the cool part is that Money Pickle doesn’t set the rates—your advisor does.

In my case, the advisor made clear that our second meeting would also be complimentary. If I wanted to move forward after that, he’d walk me through his fees and what ongoing support would look like—but only if I was interested.

So far, I don’t appear to be stuck in a sales funnel, and I never felt forced into any decision on the call. It was clear I could take the advice from the free call and walk away—or dig deeper if it felt like a good fit.

Pros and cons of using Money Pickle

-

Totally free to tryYou get a full 45-minute call with a real financial advisor at no cost. No payment info is needed, and there’s no pressure to commit.

-

Genuinely pitch-freeMy advisor didn’t mention his fees once. There was no upsell or bait-and-switch. The entire call felt like thoughtful, personalized advice.

-

Fast and easy bookingIt took me less than 10 minutes to schedule a call. I got instant confirmations and several reminders, including a phone call the day before.

-

Tailored advice from a CFP®This wasn’t generic budgeting 101. My advisor reviewed my intake responses ahead of time, asked specific questions about my finances, and gave smart, nuanced recommendations based on my goals.

-

A low-risk way to explore financial planningIf you’ve never talked to an advisor before (or feel weird about doing it), Money Pickle makes the first step easy and approachable.

-

You don’t choose your advisorYou’re matched based on your intake form, not personal preference. My match was great, but some people may prefer browsing bios first.

-

Time zone mix-up potentialI accidentally booked in the wrong time zone while traveling. It wasn’t a huge deal, but it’s something to double-check before confirming.

-

Ongoing support isn’t freeIf you want to keep working with the advisor, you’ll need to discuss their individual fees after your free call. There’s no universal pricing.

Who is Money Pickle best for?

Money Pickle isn’t trying to replace a full-service financial planning firm. Instead, it fills a specific gap: helping people take the first step.

Here’s who it’s great for:

- First-time advice seekers who aren’t sure where to begin or whether they even need an advisor

- DIY budgeters and savers who want a second opinion on their financial strategy

- People in transition—starting a business, buying a house, changing careers—who need outside insight

- Anyone nervous about getting sold to and wants to test the waters without pressure

- Busy folks who need a quick, professional gut check before making a money move

It may not be ideal for:

- People who already have an advisor and aren’t looking to switch

- Those looking for fully automated investing—this is a human advisor, not a robo-advisor

- Anyone wanting ongoing support for free—the first call is complimentary, but continued planning comes at a cost

How does Money Pickle compare to other financial planning options?

Instead of hunting down advisors, scheduling a bunch of intro calls, and hoping you click with one, Money Pickle does the matchmaking for you.

Here’s how it compares to other personal finance companies:

- Facet: Facet also offers a free intro call and connects you with a CFP®—but from there, everything stays in-house. You pick a flat-fee membership and work with a planner through Facet’s platform and dashboard. It’s a great option if you’re ready for an ongoing relationship. But if you’re just looking for a one-time gut check or want to meet an advisor before committing to anything structured, Money Pickle could be a lower-lift starting point.

- Empower: Empower blends investment management with access to human advisors. It also includes a free budgeting dashboard that helps you track your spending, net worth, and retirement goals. It’s geared toward people who are ready to review their entire financial picture and could have higher asset minimums than Money Pickle.

- Traditional advisors: The advisors you meet through Money Pickle are traditional advisors. The difference is how you get in the door. Instead of cold-emailing firms or attending awkward meet-and-greets, you get a pressure-free intro call with someone who’s already been vetted.

If you decide to keep working together, the advisor’s rates are the same as if you’d found them on your own. But the value of Money Pickle is in the ease of getting started, especially if you’re unsure where to begin.

Would I use Money Pickle again?

Yes—and I’m kind of surprised to say that. I’ve always felt quite confident handling my finances solo, but this call made me realize there’s real value in having a professional gut check. My advisor wasn’t pushy, didn’t try to sell me anything, and actually gave me insights I hadn’t considered.

If you’re curious about working with a financial advisor but don’t want to commit (or get pitched to), this is an easy way to dip your toe in—and maybe even walk away with a few aha moments of your own.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}