- No required initial draw

- Up to 2% cash back

- Excellent scores from customers on Trustpilot and Google

If you’re a homeowner in the U.S., you might have heard of Aven’s credit card. This product combines the flexibility of a credit card with the cost-saving potential of a home equity line of credit (HELOC). It allows you to unlock the value tied up in your home, offering lower interest rates than traditional credit cards. If you’re planning significant expenses, such as home renovations or debt consolidation, this could be a sensible choice.

However, our editorial team has not yet determined a rating for Aven’s HELOC credit card. It’s a relatively new product in the home equity landscape, and while it shows promise, we can’t say it’s the best option for any particular need just yet.

By opting for this card, you’ll tie your borrowing to the value of your home, which can be risky if you’re not careful with your spending. It’s best suited for disciplined borrowers with a clear understanding of home equity and the responsibilities that come with leveraging it.

About Aven

Founded in San Francisco, Aven is revolutionizing how homeowners access their equity through its unique HELOC credit cards. Unlike traditional HELOC providers, Aven offers a seamless, quick process with up to 2% cash back and no required initial draw amount.

The company aims to make financial flexibility more attainable, whether you’re looking to fund a home renovation or balance a budget. Aven may appeal most to those with a strong credit history and sufficient home equity.

Keep reading as we dissect Aven’s innovative HELOC credit card to help you decide whether this modern approach to home equity fits your financial landscape.

Aven HELOC card at a glance

We’ll dive deeper into the details listed in the table below as you read on.

| Terms | Details |

| Rates (APR) | 7.99% – 15.49% variable |

| Rate discounts | 0.25% autopay (Applies to new cardholders only; unenrolling from autopay increases APR) |

| Loan amounts | Up to $250,000 limit ($100,000 limit in specific states, listed below*) |

| Draw period | No conventional draw period; no required initial draw for lines up to $100,000

Minimum payment is 1% of principal balance plus interest and fees |

| Repayment period | No conventional repayment period (Option to refinance balance to a new account with Aven after a 15-year term if you meet underwriting criteria, or you must pay off the balance over 60 months) |

| Fees | No annual, signup, or prepayment fees

2.5% fee on cash-outs and balance transfers $29 late fee for missed minimum payment |

| Unique features | Choose fixed monthly installments for balance transfers or cash-outs

2% cash back with autopay No appraisal required |

*$100,000 limit for customers in Alabama, Alaska, Arkansas, Idaho, Iowa, Kansas, Louisiana, Nebraska, New Hampshire, New Mexico, North Dakota, Oklahoma, Oregon, South Dakota, and Wyoming.

The repayment options, combined with the absence of a formal appraisal and annual fees, make Aven’s HELOC card appealing. However, the 2.5% fee on cash-outs and balance transfers could be a drawback, depending on how you plan to use the card.

How does an Aven card work?

You can manage your HELOC via phone, online, or a handy mobile app.

Your home equity is vital. It influences your rates and the size of your credit line. Aven’s maximum combined loan-to-value (CLTV) is 89% for primary residences.

Here’s what that means: If your home is valued at $300,000 and you owe $100,000, your equity is $200,000.

Amount owed on the home / Current home value = Home equity

$100,000 / $300,000 = 33.3%

Your loan-to-value (LTV) ratio is a low 33.3%, making you a candidate for a hefty credit line. The maximum combined CLTV—mortgage balance plus your line of credit, in this case—is 89%, which is $267,000 ($300,000 x 89%).

So if you subtract the amount you owe on the home from the 89% CLTV, you could qualify for a line of credit up to $167,000:

$267,000 max CLTV – $100,000 owed = $167,000

Aven stands out because it doesn’t require a formal home appraisal, unlike many home equity lenders. Aven employs an automated system for a quick estimated home value.

Aven’s HELOC card’s flexibility and easy application process offer a modern way to access your home’s equity.

The Aven card combines a traditional HELOC with a credit card. The table below breaks down how it differs from both products:

| Feature | Aven home equity credit card | Traditional HELOC | Traditional credit card |

| Collateral required? | ✔️ (Your home) | ✔️ (Your home) | ❌ |

| Interest rates | Variable | Variable or fixed (variable is more common) | Often variable; higher than HELOC or Aven card |

| Credit line | Up to $250,000 | Varies by lender | Often lower than HELOC or Aven card |

| Cashback rewards | Up to 2% | Rarely | Varies by card |

| Application process | Automated, online | In person or online | Often online |

| Fees | Fees on cash-outs and balance transfers | Possible origination fees; annual maintenance fees; appraisal fees | Varies by card |

| Appraisal required? | ❌ | ✔️ (in many cases) | ❌ N/A |

| Repayment | Similar to credit card | Interest-only draw period (up to 10 years) | Monthly minimum payment |

| Credit score requirements | Minimum 620 | Varies by lender | Varies by card |

Who’s eligible for an Aven HELOC credit card?

Aven doesn’t disclose all the eligibility criteria for its HELOC card. Here’s what we found in our research:

| Requirement | Details |

| Properties | Primary residences, secondary homes, investment properties (additional requirements apply for the latter two) |

| State of residence | Not disclosed |

| Maximum loan-to-value | 89% on primary residences |

| Maximum debt-to-income | Not disclosed |

| Minimum credit score | 620 for primary residences |

| Minimum income | Not disclosed |

You can contact Aven for more information or see whether you prequalify on its website, but this table should give you a solid starting point.

What are the costs and fees of an Aven HELOC card?

Interest rates are a significant part of the cost of a HELOC, but consider the fees to get an accurate idea of what an Aven card will cost.

Aven offers variable interest rates between 7.99% and 15.49%. Your rate depends on factors including your credit score, loan-to-value ratio, and even your state of residence. A lower rate will make borrowing cheaper, and a higher rate does the opposite. New cardholders who opt for autopay can get a 0.25% rate discount.

As you can see in the example below, even a small rate change can have a substantial impact on the overall cost of your HELOC:

| Scenario | Without autopay discount | With autopay discount | Difference |

| Initial borrowed amount | $50,000 | $50,000 | — |

| APR | 9% | 8.75% | 0.25% |

| Initial minimum monthly payment | $875 | $864.58 | $10.42 |

| Total repayment | $94,981 | $92,449 | $2,532 |

| Time to repay | 15 years | 15 years | — |

Note: The initial minimum monthly payments would decrease as the outstanding balance goes down, unless you incur other fees or make additional charges.

Aven doesn’t charge annual or signup fees. However, you will pay a 2.5% fee on cash-outs and balance transfers, along with a $29 late fee if you miss the minimum payment.

Aven offers competitive rates and fewer upfront fees than many other lenders, but the cash-out and balance transfer fees could sneak up on you. Always read the fine print.

How do you repay a HELOC credit card from Aven?

Repaying a HELOC from Aven might feel like paying off a credit card, but we’ll further break down the repayment process so you know exactly what you’re getting.

Unlike a standard loan or a home equity loan, where you borrow a lump sum and pay it off in installments, a HELOC gives you a credit line you can draw from. With Aven, you don’t have a traditional draw period or repayment term. That offers flexibility but also requires diligence to manage costs.

No initial draw required

You’re not required to draw an initial amount for lines up to $100,000. During the period you use the line of credit, the minimum payment is 1% of the principal balance plus interest and fees. Without a conventional repayment period, you can take your time paying it back. However, if a balance remains after 15 years, you must refinance with Aven or pay off the balance over 60 months.

Choose fixed monthly installments

If you use your card for balance transfers or cash-outs, you’ll pay a 2.5% fee—but you can choose fixed monthly installments over a five- or 10-year term instead of relying on a variable rate.

No prepayment fees

Aven doesn’t charge prepayment fees, so you can pay off your HELOC early without additional costs.

The terms at Aven offer a mix of flexibility and fixed options. Whether that works to your advantage depends on how you manage the line of credit. Being strategic can result in lower costs at the end of the term.

How does your home’s value affect your terms?

The value of your home isn’t just a point of pride; it’s a pivotal factor in securing a HELOC with Aven. Because your home secures a HELOC, its value influences your terms, including the credit limit and even the interest rate.

Aven allows a maximum combined CLTV of 89% on primary residences, meaning your loan amount combined with what you owe on your mortgage can’t exceed 89% of your home’s value.

What does Aven’s appraisal process look like?

Now, let’s look at how Aven pinpoints your current home value: The lender skips the traditional in-person appraisal. Instead, it uses an automated system to estimate your home’s value, making the process faster and less intrusive.

The automated system quickens the application process. You won’t need to schedule an in-person visit or wait for an appraiser. Just provide the necessary details about your home and let Aven’s system do the rest.

Compared to the traditional appraisal methods used by many lenders, Aven’s process is faster and more convenient. But an automated system might not capture the nuances of your home’s value as thoroughly as an in-person appraisal.

Aven’s appraisal process streamlines your application, but the trade-off could be in accuracy. Always compare your options to ensure you’re getting terms that reflect your home’s worth.

Pros and cons of an Aven card

It’s crucial to weigh the good and bad to see whether Aven’s HELOC is the right fit for you. Here’s a rundown of its strengths and weaknesses.

-

Up to 2% cash backA rare perk in the HELOC space, Aven gives you a chance to earn back on your spending.

-

High credit limitIn many states, you can get a credit line up to $250,000, offering substantial borrowing power.

-

No appraisal requiredAven’s automated system means you skip the traditional appraisal, speeding up the application process.

-

No initial draw requiredYou aren’t forced to draw funds immediately, offering more flexibility.

-

No origination feesTraditional HELOCs often come with origination fees. With Aven, you avoid that upfront cost.

-

High qualifications for low ratesFor Aven’s most favorable rates, you’ll need a high credit score and substantial home equity.

-

Variable ratesThe absence of fixed-rate options means you risk higher interest costs if rates climb.

-

Cash-out and balance transfer feesUnlike some competitors, Aven levies fees on balance transfers and cash-outs, which can add to your costs.

Aven offers enticing benefits, including cash back and a high credit limit, making it a competitive option. However, the absence of fixed-rate options and fees on certain transactions can be drawbacks.

If you have a high credit score and substantial home equity, you might find lower rates elsewhere. For alternatives, consider our top-rated HELOC companies:

| Lender | Editorial rating (out of 5) | Best for |

| Figure | 4.9 | Best overall |

| LendingTree | 4.7 | Best marketplace |

| Hitch | 4.4 | Best for fast funding |

Is Aven a reputable lender?

Customer reviews can help set your expectations. Here’s a quick glance at Aven’s standing on popular review platforms:

Collected on September 21, 2023.

Aven shines on Trustpilot and Google, earning high marks for ease of applying and financial flexibility. The notary process, often a cumbersome step, gets particular praise for being user-friendly. Trustpilot and Google tend to be reliable platforms where customers can share their experiences, both positive and negative.

However, Better Business Bureau tells a different story. Aven isn’t BBB-accredited and carries a low rating there due to complaints about transparency in closing loans and unclear credit check procedures. The BBB is a well-established platform known for its strict review process, but Aven has just four reviews on BBB versus almost 3,000 on Trustpilot.

Aven garners a spectrum of opinions, from high marks for user experience and application ease to transparency issues that have raised flags for previous customers.

Does Aven have a customer service team?

Aven’s customer service team is based in San Francisco, California, where the company is headquartered. This team is your go-to for any questions or issues you may have about your HELOC, from application to repayment.

It offers a range of options to get in touch, so you can choose what works best for you:

Whether you prefer to communicate via email or like scheduling a call, Aven’s customer service aims to meet your needs.

How to apply for an Aven HELOC credit card

When it comes to ease and speed, Aven’s application process stands out. Unlike some lenders, Aven lets you prequalify to check your offer without affecting your credit score. However, a hard credit check is necessary later in the process.

Here’s how to apply for an Aven HELOC:

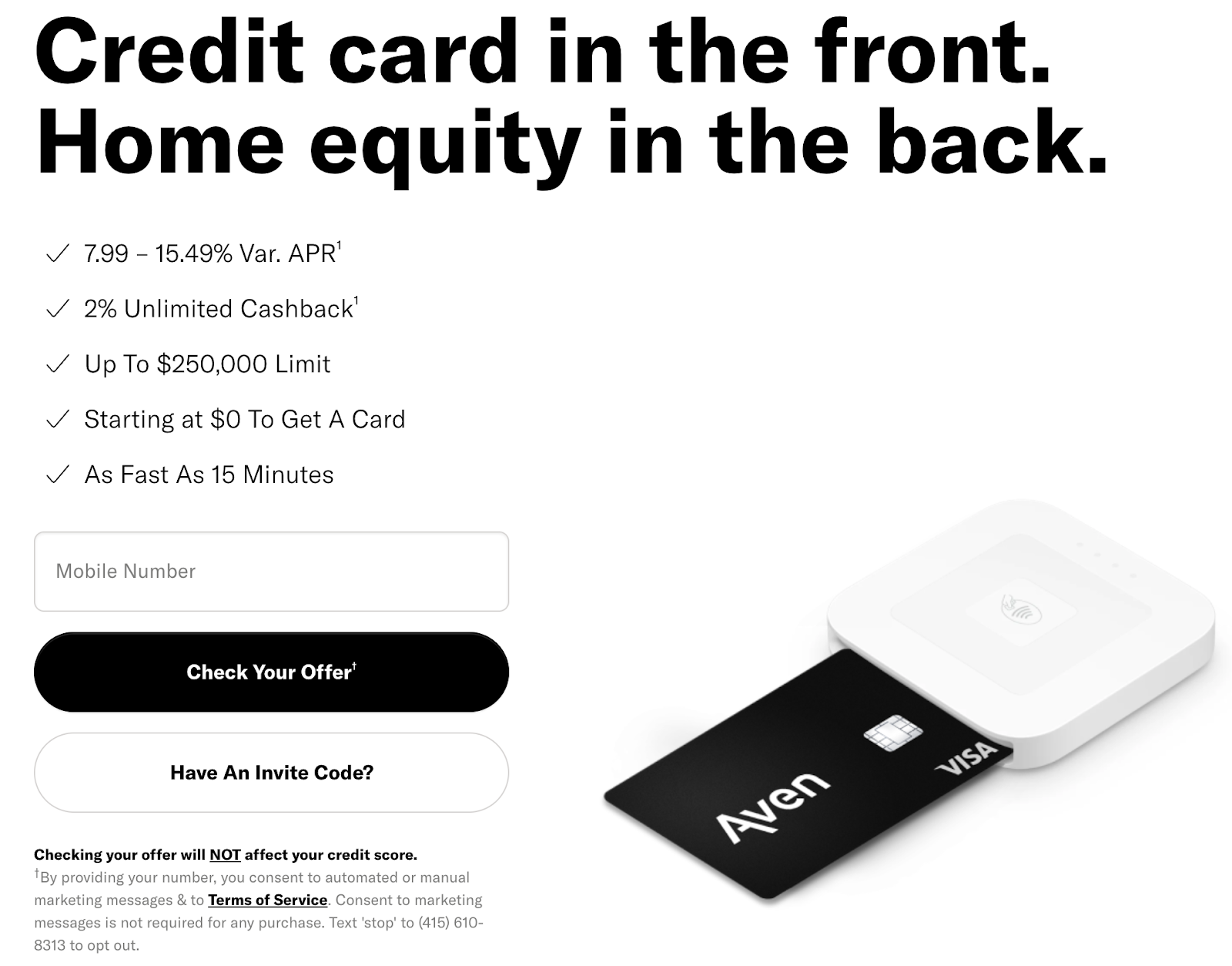

- Start the process: Go to Aven’s homepage and click “Check your offer.” Enter your mobile phone number to get started.

Source: Aven

- Confirm identity: Verify who you are and where you live.

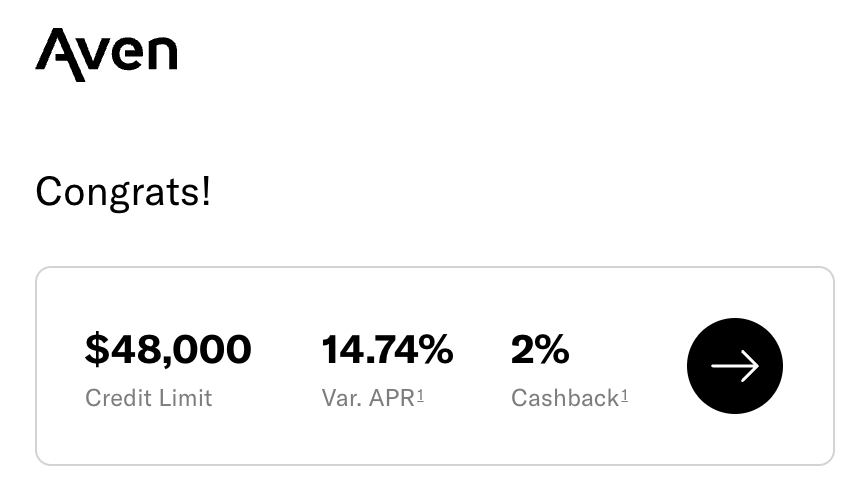

- Review your offer: Check whether you qualify, and review the terms, including your credit limit, APR, and cashback percentage.

Source: Aven

- Proceed: Click the black arrow button to move on to the next step.

- Income verification: Use bank accounts or pay stubs to confirm your income.

- Credit check and notary: Aven will do a hard credit check at this stage. An online notary will help you sign the required documents via video call.

- Get your card: Get your card and access to funds within 10 business days.

Aven makes applying for a HELOC straightforward. Just prepare for the hard credit check, and ensure you have your income verification documents handy.

What if I’m denied a HELOC card from Aven?

If Aven turns down your HELOC application, you can reapply after a six-month waiting period. However, Aven doesn’t offer manual overrides; its underwriting system is fully automated.

The lender should notify you by mail why it denied your application.

Here are four common reasons for denial and next steps:

- Low credit score: Improve your credit by paying bills on time and reducing debt.

- Insufficient income: Boost your income or reduce other debt to improve your debt-to-income ratio.

- High debt obligations: Pay down other debts to improve your financial standing.

- Low home equity: Build more equity in your home before reapplying.

Given that Aven’s system is automated, understanding these pitfalls can help you make necessary improvements before you try again.

Also, remember: Aven isn’t the only home equity company. Consider prequalifying with others, starting with our top-rated HELOC and home equity loan lenders.

How do other home equity products compare to Aven?

Unlike a home equity loan, which gives you a lump sum upfront with a fixed repayment schedule, Aven allows you to draw money as needed and only pay interest on what you’ve borrowed. This offers flexibility a home equity loan doesn’t provide.

Reverse mortgages and cash-out refinances are other routes homeowners often consider. A reverse mortgage is generally for older homeowners and turns home equity into regular payments, with the loan balance due upon certain life events, such as selling the home or the owner’s death.

A cash-out refinance replaces your mortgage with a larger one, handing you the difference in cash. Both differ from Aven’s HELOC, which doesn’t require you to replace your mortgage and may be more cost-effective in terms of closing costs and interest rates.

Aven card FAQ

How long does it take to receive funds from Aven?

After you apply for an Aven HELOC card, the approval process involves a few steps, such as confirming your identity and income. The process is quick, often culminating in an online notary session to sign the required documents.

After the formalities, you can generally expect to get your card and access to your funds within 10 business days.

Do you need to tell Aven what the funds are used for?

During prequalification, you have the option to select the purpose: home improvements, a balance transfer, or “other.” Your choice doesn’t appear to affect your eligibility, and Aven doesn’t seem to put strict limitations on fund usage.

Does Aven have insurance requirements?

We couldn’t find specific information on Aven’s website about insurance requirements for obtaining a HELOC. In general, lenders may require certain types of insurance, such as homeowner’s insurance, but we can’t confirm this for Aven.

Can you back out of a HELOC card?

The ability to back out of a HELOC contract with Aven depends on what stage you’re in. During the application process, you’re not locked into anything. If you’ve been approved but haven’t gotten the funds, you likely still have an option to back out.

Once you receive the funds, the contract is generally binding, and specific conditions will apply for cancellation or closure.

Can you close your Aven account at any time?

If you wish to close your Aven HELOC account, you’ll send a payoff letter to [email protected]. Once you’ve paid off all balances, Aven will process the liens and close your account.

Specific terms might apply, so it’s best to read your contract to understand any penalties or conditions for early termination.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}