[ad_1]

Teaching your teen how to manage money is one of the most impactful lessons you can pass on before adulthood. With the proper foundation, they’ll build confidence, avoid common financial pitfalls, and make informed decisions for years to come.

This guide gives you a roadmap for supporting your teen through key milestones, such as earning money, budgeting, banking, saving, building credit, and investing. You’ll also learn how to set financial goals and reinforce positive habits through real-life practice.

Table of Contents

Why high school is the best time to teach your teen about money

Teens make money decisions all the time—how to spend birthday money, whether to save for a goal, or if they can afford to go out with friends. These daily choices shape how they view and manage money for years. Without early financial education, teens are more likely to carry poor habits into adulthood.

Schools often don’t teach it

Personal finance is often left out of high school curricula despite its importance. According to the Council for Economic Education’s 2024 Survey of the States, only 35 states require high school students to take a course in personal finance. Even when courses exist, the content may be limited or inconsistently delivered.

This leaves many teens unprepared for real-world financial tasks. They might graduate knowing how to solve algebra problems but not how to open a checking account, understand a paycheck, or compare loan options.

The consequences of financial illiteracy

Young adults are more vulnerable to debt, financial stress, and poor money management without these skills. A study from FINRA shows that adults with low financial literacy are more likely to carry credit card debt, pay late fees, and struggle to build savings. Many of these patterns begin in the teen years.

Parents play a key role

If schools aren’t teaching these lessons, parents have an opportunity to step in. You can tailor financial discussions to your teen’s interests and use everyday experiences to model good decision-making. Reviewing bills together, setting a savings goal for a summer trip, or comparing prices while shopping can all be informal but powerful lessons.

Helping your teen understand money also builds character. Teens who manage their own budgets learn responsibility, patience, and how to set priorities. These skills benefit them in school, relationships, and future career choices.

The most impactful money lessons start with you

Talking about money at home helps teens build financial confidence long before they face major decisions. Yet many families avoid these conversations, either to protect kids from financial stress or due to personal discomfort. Silence, however, often leads to confusion, missed learning opportunities, and inherited bad habits.

Open, age-appropriate dialogue has lasting benefits. Teens who discuss money with their parents are more likely to budget, save, and make responsible financial choices. These conversations normalize financial decision-making and help teens feel capable and prepared.

Start with your own money habits

One of the most effective ways to teach is by example. If your teen sees you budgeting, saving, or making thoughtful spending choices, they’ll naturally pick up on those habits. You don’t need to be perfect. Honest conversations about past financial mistakes can be just as impactful.

Use real-life moments to share your financial thinking.

We’re eating in more this month so we can save for a trip.

We chose not to finance a car to avoid paying interest.

These examples help teens connect values to behavior.

Introduce a teen allowance with a purpose

A monthly allowance can be your teen’s first real-world experience managing money. Give them a fixed amount and let them decide how to budget it, even if that means learning from small mistakes. Letting them feel the consequences of overspending now builds better habits later.

Introduce a basic structure like spending, saving, and giving categories to guide their thinking. This teaches them to prioritize and set goals without making the process restrictive. If your teen has a job, treat their earnings similarly and help them plan for ongoing costs like gas or phone bills.

Create a habit of budget check-ins

Make money conversations a routine, not a lecture. Schedule a monthly check-in where your teen reviews their spending with you. Ask how they made certain choices and what they might do differently next time.

You can also involve them in the family budget. Show them how much groceries, streaming subscriptions, or electricity actually cost. Then, ask them to help identify ways to cut back or set savings goals for shared expenses.

Use this time to discuss needs versus wants and turn everyday spending into teachable moments.

Was that worth the cost?

Would you make that same purchase again?

Talk about goals, not just rules

Rather than focusing on what they can’t buy, ask your teen what they want to achieve. Then help them map out a savings plan and timeline. Setting personal goals makes budgeting feel empowering rather than limiting.

Let them think big—whether they want to save for a concert, a new phone, or college expenses. Turn those dreams into clear targets, and use trackers, charts, or apps to make progress visible and motivating.

How earning money builds responsibility and independence

When teens start earning on their own, they gain more than just spending money. They build responsibility, confidence, and awareness of how hard-earned dollars are spent.

These experiences encourage smarter financial decisions because the money isn’t handed to them—it’s earned. Even small earnings can teach lasting lessons.

Why earning early matters

A part-time job or side hustle teaches more than basic money skills. It helps teens develop time management, communication, and customer service skills they’ll use in college and beyond. Earning also builds confidence, showing them they’re capable of handling responsibilities typically reserved for adults.

The goal isn’t to replace a full-time income. It provides a low-stakes environment where they can learn how to balance work, money, and personal priorities. Whether babysitting for neighbors or picking up freelance projects online, each experience builds toward financial maturity.

Job options for high school students

Today’s teens can access traditional jobs and flexible, digital-era income streams. Various options suit different personalities and schedules, from babysitting and retail work to tutoring and reselling clothes online.

| Opportunity | Age Requirements | Average Pay | Flexible |

| Babysitting | 13+ | $12/hr | ✔️ |

| Tutoring | 14+ | $15-$25/hr | ✔️ |

| Retail or service jobs | 16+ | $10-$15/hr | ❌ |

| Freelancer | 13+ (w/ parent) | Varies | ✔️ |

| Yard work or pet sitting | 12+ | $10-$20/hr | ✔️ |

Before starting any job, review local labor laws to ensure your teen’s work is legal and appropriate for their age. Federal guidelines limit 14- and 15-year-olds to 3 hours of work on school days and 18 hours during the school week.

What to do with that first paycheck

A first paycheck is a teachable moment. Review the pay stub together and explain gross pay, taxes, and deductions like Social Security and Medicare. This sets the stage for understanding income and budgeting.

Encourage your teen to divide earnings into three categories: saving, spending, and giving. This framework helps them learn how to prioritize needs, wants, and generosity. Suggest setting aside a portion each month for an emergency fund—even $10 per paycheck adds up and creates a safety cushion.

Goal-setting can also make work more motivating. Whether saving for a phone or putting money toward college, connecting earnings to goals gives their job more purpose.

Encouraging entrepreneurial thinking

Not every teen fits into a traditional job, and that’s perfectly fine. Encourage them to test small business ideas like selling handmade items, editing videos, or running a neighborhood lawn care service. These ventures build creativity, independence, and problem-solving skills.

Let them experiment and even fail. Trial and error teaches adaptability and resilience. Whether they earn $20 or $200, they’re learning how to create value and manage the money that follows.

Why budgeting builds confidence and smarter choices

Budgeting gives teens control over their money and the confidence to manage it responsibly. With a plan in place, they’re less likely to overspend, more likely to meet their goals, and better prepared for future financial responsibilities.

Without a budget, money disappears quickly. A paycheck can vanish over a weekend with little to show for it. Budgeting assigns purpose to each dollar and helps teens make decisions they won’t regret later.

Why budgeting builds confidence

Budgeting isn’t about restriction—it’s about choice.

Teens learn to align spending with what matters to them, whether saving for a car or setting aside money for gifts. The sooner they get into the habit, the more empowered and less stressed they’ll feel around money.

A simple spending log can reveal patterns and help your teen make more thoughtful decisions. Budgeting also permits them to say no to unnecessary expenses because they know what they’re working toward.

Teach the 50/30/20 rule

A great starting point is the 50/30/20 rule, which divides income into three categories:

- 50% for needs (e.g., gas, basic phone plan)

- 30% for wants (e.g., streaming, snacks, entertainment)

- 20% for savings or debt (e.g., emergency fund, future goals)

Even if your teen isn’t earning much, this rule works by focusing on percentages, not dollar amounts. To illustrate the concept, try applying it to a recent allowance or birthday gift.

Let them adjust the split based on their life stage. A teen with minimal expenses might save more than 20%, while one with car insurance or school costs might allocate more to needs. The goal is to get them thinking critically about how they divide their money.

Use apps or paper, but always track

Tracking spending is the most important habit to build. Whether your teen prefers a budgeting app, spreadsheet, or notebook, they need a consistent system. Writing down every expense builds awareness and curbs impulse purchases.

Here are a few tools:

| App Name | Best for | Free Version |

| You Need a Budget | Detailed planning | No |

| Greenlight | Teen budgeting & parental tools | Limited |

| GoHenry | Kids and teens | No |

| Spending Tacker | Simple logging | Yes |

Some teens prefer visuals like color-coded whiteboards or printed trackers, while others may want reminders on their phones. Let them choose the method that fits their style, but encourage consistency over perfection.

Practice with real-life examples

To make budgeting stick, build a sample budget together. Start with their total income, then list fixed and flexible expenses, like Spotify, weekend activities, or planned savings.

Use this exercise to show how their money flows and where they can adjust.

Ask questions to spark reflection:

- What are you saving for?

- Was this purchase worth it?

- Would you rather spend now or save for something bigger?

These conversations help tie numbers to priorities and goals.

Reinforce good habits

Celebrate the small wins, such as sticking to a weekly limit or reaching a short-term savings goal. Recognition boosts motivation and helps make budgeting feel like progress, not punishment.

Why every teen needs a bank account they can manage

A bank account is often a teen’s first real step toward financial independence. It teaches them how to manage deposits, withdrawals, and digital tools they’ll use for life. With guidance, they can learn how to use a debit card, track balances, avoid overdrafts, and build saving habits that stick.

Banking also helps shift how teens think about money. When cash is stored in a wallet, it disappears quickly. But when they can view transactions, set alerts, and watch their balance grow, they become more mindful about how they spend.

Choosing the right type of account

There are a few account structures to consider for teens. Most banks offer joint teen checking accounts, where the parent is a co-owner. This provides visibility and control, while allowing the teen to use the account as needed.

Some institutions also offer custodial accounts, which remain under parental control until the teen reaches adulthood (usually age 18 or 21). These are more restrictive and often better for long-term savings than regular spending.

Ideally, teens should have a checking account for spending and a savings account to grow longer-term funds. This setup teaches how to manage two goals simultaneously—what they need now, and what they’re building for later.

Look for the following features:

- No monthly maintenance fees

- A mobile banking app with notifications

- Parental monitoring tools

- Free ATM access

- A debit card with spending limits

Some excellent banking options

| Bank | Product | Features |

| SoFi | ||

| Varo | ||

| Chime | ||

| Mercury |

Teaching bank account basics

Once the account is open, show your teen how to log in, check their balance, and read transactions. Explain how debit card purchases work, and what happens if there isn’t enough money in the account.

Discuss how to use ATMs wisely. Talk about avoiding fees, checking account balances before withdrawing, and what to do if they lose their card. To stay informed, encourage them to set up alerts for low balances or large transactions.

It’s also important to explain the difference between debit and credit. Many teens assume they’re interchangeable, but only credit cards impact credit scores. Understanding this now helps avoid confusion later.

Make it a learning experience

Encourage your teen to deposit their paychecks or allowance instead of using cash. Set up recurring transfers into savings or introduce envelope-style budgeting within their digital tools. Seeing their balance grow—slowly and steadily—makes the value of saving real.

Make account reviews part of your monthly check-ins. Ask your teen to explain recent purchases, transfers, or goals. These moments reinforce their learning and open the door for deeper conversations about financial choices.

Opening a bank account is more than a transaction. It’s a foundation for future financial habits and gives your teen a sense of ownership over their money. With the right support, it becomes a powerful tool for growth.

Help your teen build credit with confidence

Credit scores affect nearly every major financial decision in adulthood, from getting approved for a loan to renting an apartment. Helping your teen understand credit early on can prevent future missteps and give them a head start in building healthy financial habits.

Though your teen may not use credit today, they’ll need a strong score soon—whether to qualify for student loans, open a credit card, lease a car, or apply for housing.

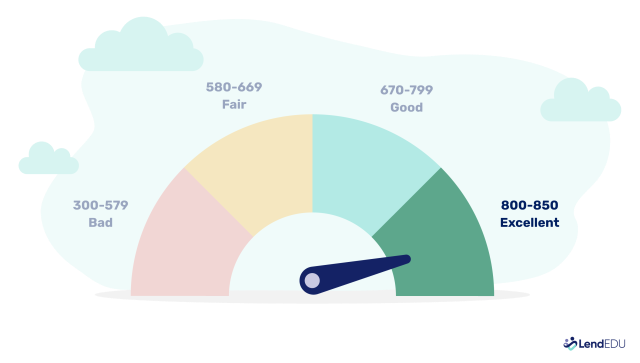

What is a credit score?

A credit score is a three-digit number representing a person’s financial reliability. Most scores range from 300 to 850, with higher scores signaling greater creditworthiness. In the U.S., most lenders use the FICO or VantageScore models, which evaluate similar factors to determine someone’s risk level.

Even though your teen might not have a score yet, learning how one works prepares them to build credit responsibly from the start. A single missed payment at 18 could still impact their credit report well into their mid-20s.

Why teens should learn early

Credit is one of the most misunderstood aspects of personal finance. Many teens associate it only with debt or “free money.” Teaching them early shows that credit is a tool and not something to fear.

Learning how credit works allows your teen to:

- Recognize the difference between good debt (e.g., student loans, secured credit cards) and bad debt (e.g., payday loans)

- Understand the long-term consequences of financial decisions

- Build a credit history gradually before it’s urgently needed

Early knowledge also positions your teen to access better loan terms, lower interest rates, and more approvals in the future.

What makes up a credit score

The FICO score model, used by most lenders, is based on five key factors:

- Payment history (35%) – Do you pay bills on time?

- Credit utilization (30%) – What percent of your credit limit are you using?

- Length of credit history (15%) – How long have your accounts been open?

- Credit mix (10%) – Do you use a variety of credit types (e.g., loans, cards)?

- New credit inquiries (10%) – How often do you apply for new credit?

The first two categories carry the most weight. Emphasize that paying bills on time and keeping balances low are the most effective ways to build and protect credit.

Tools to help teens start building credit

Once your teen understands how credit works, learning how to build it safely is the next step. While most credit-building products require applicants to be at least 18, there are beginner-friendly tools that allow teens to take early, low-risk steps. The focus isn’t just on raising a score—it’s about forming habits that support long-term financial success.

1/ Becoming an authorized user

One of the easiest ways to help your teen start building credit is by adding them as an authorized user on your credit card. This means they’ll receive their own card tied to your account, while you retain responsibility for the bill.

If the primary cardholder (you) pays on time and keeps balances low, that positive activity may be reflected on your teen’s credit report. However, not all credit card issuers report authorized user data to the credit bureaus, so contact your issuer to confirm.

If you choose this route:

- Set clear spending rules together

- Use the card for predictable, budgeted expenses (like gas or groceries)

- Review statements each month to talk through purchases and payment behavior

This setup allows teens to learn while you remain in control of the account.

2/ Applying for a student or secured credit card

At age 18, your teen can apply for a credit card independently, often with a co-signer or proof of income. Two popular starter options include:

- Student credit cards – Designed for first-time users with little to no credit history. They typically come with low limits, no annual fees, and basic rewards.

- Secured credit cards – Require a refundable security deposit (usually $200–$500) that acts as the credit limit. These are easier to qualify for and still report activity to all three credit bureaus.

If you’re just beginning to build or repair your credit history, I recommend considering a secured credit card, which requires a refundable deposit and helps build credit through on-time payments. It’s a low-risk, practical first step. I also suggest using an app that reports rent and utility payments to credit bureaus, especially for renters, so those consistent payments can help your credit score.

Here’s a comparison of beginner credit cards:

| Provider | Product | Type | Age Requirement | Highlights |

|---|---|---|---|---|

| Discover | Student Cash Back | Student card | 18+ | 5% cash back, no annual fee |

| Petal | Petal 1 | Unsecured card | 18+ | No credit history required |

| Capital One | Secured Mastercard | Secured card | 18+ | Reports to all 3 bureaus |

| Experian | Experian Go | Credit file builder | 13+ | Uses bill payments to establish credit file |

Before applying, review terms together. Compare fees, interest rates, and whether the card reports to all three credit bureaus (Experian, Equifax, and TransUnion). Start with a low limit and clearly define what types of purchases are allowed.

Using credit responsibly

Once your teen has a credit-building tool, it’s essential to reinforce best practices:

- Keep credit utilization below 30%. For example, if the limit is $300, stay under $90 in total balance.

- Always pay on time. Even one late payment can hurt their score and lead to fees.

- Pay in full when possible. Carrying a balance triggers interest charges and can lead to debt.

Encourage your teen to pause before using credit and ask, “Would I still want this if I had to pay cash?” Framing credit as a convenience—not a source of extra money—helps build discipline.

Monitoring progress and staying accountable

Many banks and apps offer free credit score monitoring, even for new users. Consider:

These platforms offer regular score updates, explanations of changes, and suggestions for improvement. Reviewing their score monthly helps your teen understand how small behaviors impact their long-term credit health.

Helping your teen turn wants into savings goals

Saving money is more than just putting cash aside. It’s about learning discipline, planning, and patience. When teens save with a clear purpose, they begin to understand how financial decisions shape their future.

Even small amounts matter. Teens can practice saving intentionally with allowances, birthday money, or earnings from part-time jobs. The habit, not the dollar amount, builds long-term financial success.

Why teens should save with a purpose

Saving becomes powerful when tied to something your teen cares about. A new phone, concert tickets, or their first car can make the process feel motivating instead of restrictive. This shift in mindset—from saving out of obligation to saving for a reward—helps teens take ownership of their financial decisions.

It also teaches delayed gratification. Instead of spending impulsively, teens learn to weigh trade-offs and prioritize their goals.

Types of financial goals

Introduce your teen to three types of goals:

- Short-term (0–3 months): Event tickets, new shoes, a class gift

- Medium-term (3–12 months): A bicycle, holiday gifts, or a summer trip

- Long-term (12+ months): A car, college expenses, or moving costs

Ask your teen to choose one goal in each category. Help them break down the total cost and calculate a weekly or monthly savings target. For example, saving $10 a week could fund a $120 summer concert ticket in three months, turning a vague wish into an actionable plan.

Tools that encourage saving

There are several apps and banking tools that make saving easier and more fun for teens. Many offer visual trackers, savings “buckets,” and automation features that reinforce consistency.

| App/Bank | Features | Best For |

|---|---|---|

| Greenlight | Goal tracking, parent controls | Kids and teens with debit cards |

| Fidelity Youth Account | Save + invest, parental link | Teens 13–17 with parent accounts |

| Chime | Round-ups, auto-savings | Young adults (18+) |

| Current | Parent-linked savings pods | Teens earning income |

Let your teen choose the method that fits their style—consistency matters most.

Matching and motivation

To boost motivation, consider offering a parent match. If your teen saves $100 toward a bike, you might contribute $25 or $50 to reward their effort. This mimics real-world incentives like employer 401(k) matches and shows that saving can have additional benefits.

Celebrate milestones. Take a moment to recognize their progress, whether they’re hitting a halfway point or reaching the whole goal.

After a goal is met, reflect together. What worked well? What was hard? What would they do differently next time? These questions reinforce learning and build self-awareness.

Planting the seeds for smart investing habits

Investing might feel too advanced for high school, but it’s one of the most important financial skills teens can learn. When introduced early, investing helps teens see the difference between saving and growing money.

You don’t need to cover every investing term or strategy. Focus on key concepts like risk, reward, diversification, and compound growth. These ideas set the stage for smarter financial decisions later.

Core principles teens should know

Start by defining investing: using money to buy something you expect to grow in value.

Popular investment vehicles include:

- Stocks – Shares of ownership in a company

- Mutual funds – Pooled investments managed by professionals

- Index funds – Baskets of stocks that track a market index (like the S&P 500)

- ETFs – Exchange-traded funds that behave like index funds but trade like stocks

Introduce compound interest using simple examples. Show how investing $1,000 at a 7% annual return could grow to over $3,800 in 20 years. Use a calculator like Investor.gov’s compound interest tool to run different scenarios.

Then explain risk vs. reward. Stocks may offer higher returns but fluctuate more. Bonds or savings grow more slowly but carry less risk. That’s why diversification—spreading investments across types and industries—is key to managing risk while building wealth.

Stress that investing is not a shortcut to riches. It rewards consistency and long-term planning, not lucky bets or market timing.

Best ways for teens to get started

Teens under 18 can’t legally open their own brokerage accounts, but they can invest through a custodial account, managed by a parent or guardian. These accounts allow the adult to oversee decisions until the teen reaches adulthood (usually 18 or 21, depending on the state).

Here are beginner-friendly platforms:

| App/Service | Type | Custodial Option | Features |

|---|---|---|---|

| Fidelity Youth Account | Brokerage | ✔️ | Real-time stock trades, education tools |

| Acorns Early | Micro-investing | ✔️ | Rounds up purchases to invest |

| UNest | Goal-based investing | ✔️ | Gifts from family and friends |

| Stash | Beginner investing | ✔️ (via Stash+ plan) | Investing + financial literacy tools |

Practice with simulations first

If your teen isn’t ready to invest real money, start with a free stock market simulator:

Simulations let teens explore without risk. Walk through how stock prices move, what happens during a market dip, and how dividends work. You can even create a family challenge: give everyone a fake $10,000 portfolio and track progress monthly to see who makes the most informed choices.

Reinforce long-term thinking

Remind your teen that successful investing isn’t about reacting to trends or hot stock tips. It’s about staying consistent. Share stories like Warren Buffett’s early investments to emphasize how time in the market matters more than timing the market.

Use practical examples to connect investing with goals. If they save and invest $20 a week starting at 16, they could have thousands saved for a first apartment or student loan repayment by graduation.

Teaching financial safety and scam avoidance

Financial literacy isn’t just about spending and saving. It’s also about protecting money in a digital world. As teens begin managing finances online, they become potential targets for scams, phishing attempts, and identity theft. Teaching financial safety early gives them the tools to spot danger and act confidently.

Teens are often active online but unfamiliar with the warning signs of fraud. By building smart digital habits now, they’ll be better equipped to navigate apps, websites, and platforms that involve their personal and financial data.

Why safety matters in a digital world

Teenagers manage more online accounts than ever before, from banking and payment apps to gaming and social media. That increased access also comes with risk. Criminals know that teens are new to managing money and often willing to trust too quickly.

While fear isn’t the goal, awareness is. A teen who understands how to recognize, avoid, and report fraud will be far more resilient when facing real-world financial threats.

Common financial scams that target teens

Scams aimed at teens often follow familiar patterns. Share examples and walk through real scenarios to reinforce the warning signs.

- Phishing emails and texts. Messages that appear to come from banks, schools, or retailers asking for personal info or login credentials. They often contain urgent language or suspicious links. Teens should never click or respond. See FTC phishing advice.

- Fake job offers. Scammers post jobs on social media or job boards offering quick money. After “hiring,” they ask for bank info to send payments or request the teen buy gift cards for “training.”

- Scholarship and grant scams. Fraudulent organizations claim your teen has won a prize but request a processing fee or credit card number to release the funds. Legitimate scholarships are free to apply for and don’t require payment to claim awards.

- Marketplace fraud and seller scams. Teens may try to buy concert tickets, shoes, or electronics online. Scammers ask for payment via untraceable methods (like Venmo or Cash App) and disappear. Encourage shopping only through platforms with buyer protection, like eBay or Amazon.

Refer to the Federal Trade Commission’s Scam Alerts for examples you can share.

Creating safe digital habits

Good cybersecurity starts with small, repeatable actions. Help your teen build strong habits that protect their money and identity:

- Use long, unique passwords for each account.

- Enable two-factor authentication (2FA) whenever possible.

- Avoid accessing financial accounts on public Wi-Fi.

- Keep device software updated and run antivirus scans regularly.

- Never share PINs or login credentials.

Reinforce that it’s okay to ask for help

Even cautious teens make mistakes. Scammers are increasingly sophisticated, and it’s easy to fall for a well-crafted email or fake site. The most important thing is that your teen knows they can come to you without fear of judgment or punishment.

Building momentum with milestones and rewards

Financial education works best when teens can see their progress. Setting short-term goals gives structure to the learning process and helps teens stay motivated. When milestones are clear, achievable, and tied to real skills, they create momentum that builds confidence.

Why milestones help teens stay motivated

Milestones serve as practical stepping stones. They break bigger concepts into manageable tasks, providing a roadmap your teen can follow. That structure makes financial learning more interactive, especially when paired with recognition.

Examples of milestones that build financial skills

Choose milestones that align with everyday life. Here are a few examples to consider:

- Open a teen checking account with parental supervision

- Track spending for 30 days using an app or spreadsheet

- Create and follow a simple monthly budget

- Set and contribute to a personal savings goal

- Review and understand a pay stub from part-time work

- Pay a recurring expense (like a portion of their phone bill)

- Make a purchase decision after price or product comparisons

- Read and explain the parts of a credit card or bank statement

- Learn how to report a lost debit card or dispute a charge

- Set a long-term goal that includes an investment or savings plan

Encourage your teen to add their own ideas to the list. Personalizing milestones gives them more control and makes financial education feel relevant instead of assigned.

Use incentives to reinforce progress

Milestones are powerful, but incentives add an extra layer of motivation. Rewards don’t need to be monetary. What matters most is acknowledging effort and reinforcing consistent habits.

Here are some incentive ideas:

- Match a portion of their savings toward a goal

- Offer a one-time bonus for completing a budgeting challenge

- Let them control a discretionary budget for a day

- Unlock a non-monetary privilege, like a later curfew or more screen time

- Celebrate with a family dinner or a small recognition gift

If your teen prefers structure, you can create a point system where each milestone earns credits toward a larger reward.

Make goal setting SMART

Turning abstract goals into clear, trackable objectives helps teens stay focused. Use the SMART framework:

- Specific: What exactly do they want to achieve?

- Measurable: How will they track progress?

- Achievable: Is it realistic based on their income or time?

- Relevant: Does it align with what matters to them?

- Time-bound: When do they want to reach the goal?

For example: “Save $300 for a new bike by June 1 by putting away $25 per week.” This goal has a defined purpose, timeline, and action plan.

Celebrate and reflect

When your teen reaches a milestone, pause to celebrate. Recognize the work it took, not just the outcome. Ask questions like:

- “What part of this was harder than expected?”

- “What decision are you most proud of?”

- “What would you change next time?”

These reflections build financial resilience. They show your teen that success isn’t about perfection but progress, adaptability, and learning.

Your guidance today builds their financial future

Teaching teens how to manage money isn’t a one-time lesson—it’s a journey built through patience, practice, and everyday experiences. By starting during high school, you’re giving your teen a head start in learning to make smart, confident choices about their financial future.

The goal is to build a strong foundation and reinforce it over time. As a parent, your role is to offer guidance, encouragement, and the right tools so these lessons grow into lifelong habits.

Reinforcing what they’ve learned

By this point, your teen should have been introduced to key financial concepts, including:

- How to earn money and understand a paycheck

- How to create a budget and track spending

- How to open and manage checking and savings accounts

- How credit scores work and how to build credit responsibly

- How to set meaningful savings goals and begin investing

- How to avoid scams and stay safe online

- How to set milestones and celebrate progress

They won’t master everything right away—and that’s okay. Financial literacy is a skill developed through repeated exposure and real-world application. Your continued support will help these concepts take root and evolve.

Whenever possible, involve your teen in practical financial tasks. Invite them to help compare cell phone plans, evaluate travel expenses, or review a restaurant receipt. Ask their opinion during family financial conversations to build their confidence and critical thinking.

Continued support to stay on track

To stay connected and informed, sign up for the LendEDU newsletter.

It’s designed to support families like yours with up-to-date financial insights, product comparisons, and actionable advice.

[ad_2]